The API Economy And Its Role In Our Lives

We live in a period that will be defined by the expansion of connectivity in our lives. It is the factor that governs the exponential increase in the speed of change for tech adoption. It is reshaping society and our relationships with the institutions that underpin it.

The API economy is the natural next step in this process and Open Banking is important because it’s the tipping point that is bringing the API economy to life in financial services.

What Is An API?

An API, or application program interface is a set of tools and protocols that allows software applications to be controlled. It allows one application to send information and instruction on what to do, to another application. Take, for example, the Twitter API. If you use Twitter, you probably have the Twitter app on your phone. The Twitter app sends the text of your tweet and instructions to post that tweet to your timeline to the Twitter API. It’s the same with City mapper. It uses the TFL API to understand the state of the transport system. The Open Banking APIs are similar, except instead of getting text data into the twitter platform, they allow you to get transaction data from your bank into other apps and services.

Why Are They Important In Finance?

Because, on average, people have around seven financial products in their lives. They’re stressed and anxious about money and they don’t want to have to check seven different apps to stay on top of their finances. In fact, they want to avoid that so much that they’d rather not check their finances at all – this is what we call the ‘Apathy Penalty’. It’s those people who are penalised because they’re disengaged.

Loyalty Penalty

In 2018, the Consumer Markets Authority (CMA) started to investigate a super-complaint made by Citizens Advice into the same area: the penalty that you pay because you’re a ‘loyal customer’ – I’m not sure that’s a helpful name. Data from research we’ve conducted shows comparatively low levels of trust in institutions, so there seems to be no basis for calling it a penalty-relating loyalty. Perhaps the ‘Apathy Penalty’ would be a better name. No matter what you call it, it’s big – around £4.5bn according to the CMA.

APIs are important because they enable financial systems from regulated providers to talk to each other securely and, when this is possible, we start to unearth all kinds of possibilities when it comes to overcoming the barriers of customers’ apathy towards their own financial well-being.

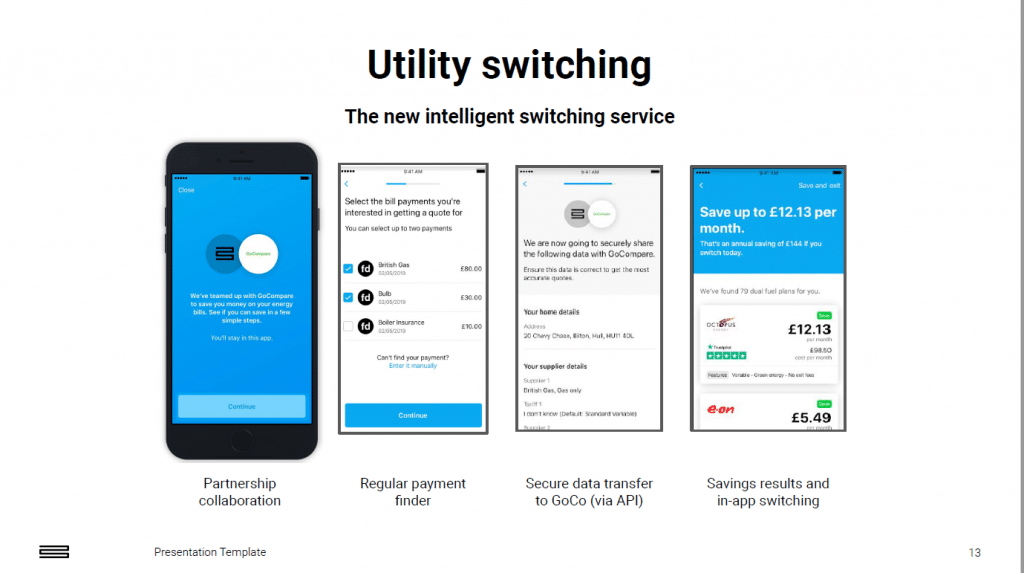

Imagine, for example, a situation in which your bank could use the data in your account to spot a utility bill that seemed high. It could then use APIs to query your supplier to find out what tariff you’re on, go to a price comparison site and get you a better quote from another supplier and, given all of the ID checks you’ve gone through to set up a bank account in the first place, it could even complete the switching journey for you.

From a user perspective it would appear something like this: I get a notification from my bank app saying my energy bill is higher than last month and asking if they can have my permission to use my personal data to see if they can find a better supplier. I say yes and 30 seconds later I’m presented with a screen with several quotes from energy suppliers alongside the suppliers “TrustPilot” score (available from another API). I select a quote and tell my bank that I’d like to switch to the provider and that’s done.

That is the power of the API and the reason the industry is talking so much about the API economy – through this new paradigm in connectivity we can offer experiences that couldn’t have been conceived of even 5 years ago. Watch the presentation all about it here.